US Rates: Term Funding Premium and the Term Structure of Swap Spreads

US Rates: Term Funding Premium and the Term Structure of Swap Spreads

We're taking a deep dive into the podcast episode "US Rates: Term Funding Premium and the Term Structure of Swap Spreads" by Srini Ramaswamy1 and Ipek Ozil2. I not only transcribed the 3, but I also added my own analysis and insights to provide an even more comprehensive understanding.

Attention: Copyright 2024, JPMorgan Chase and Company, all rights reserved. This episode was recorded on May 2nd, 20244.

What are the swap spread ?

In the US markets, the convention is to define a swap spread as the swap yield minus the US treasury. So for example, a five-year swap spread would be the five-year swap yield minus the five-year on-the-run treasury note yield. But ever since SOFR replaced Libor as the short rate benchmark in the swaps market, that has changed the very essence of what swap spreads are.

Swap spread represents actually a kind of term premium

We made the connection between swap spreads and term premium. But now the benefit is we have a few more years of historical data under our bells. The term premium affects swap spreads at every single maturity. It actually affects long end spreads more than it does short end spreads. If you focus on the term structure, you can extract information about term premium. And conversely, if you focus on term premium or term funding premium, you can adopt what we call a term structure first approach to thinking about swap spreads and modeling swap spreads. And we think by doing that, you should be able to do a better job with respect to forecasting that.

What is the term funding premium?

I would like to start is actually to look at the treasury floating rate notes or the FRN market. So treasury FRNs are basically two year maturity instruments and they pay returns that are linked to three month table. So they actually pay three month table returns every three months plus a spread. And basically over the life of this instrument, if you held it, your returns will be very similar to owning bills and rolling them every quarter for a two-year period, but you'll actually earn an additional spread on top of that. Now, why do you earn this additional spread? It's because the investor is lending money to the US Treasury for two years upfront instead of lending it for three months at a time and then rolling it every quarter. So the additional return, the market price is in. The committing principal amounts to a longer duration. That's what we refer to as term funding premium.

My Notes

The term premium is the excess return that an investor obtains in equilibrium from committing to hold a long-term bond instead of a series of shorter-term bonds.

The term premium may be negative5

The term funding premium and its link to swap spreads

Let's start by reflecting on what a 10-year swap yield and a 10-year treasury yield actually are. So SOFR is a risk-free overnight rate, which means the 10-year swap yield basically reflects the market's expected return from rolling overnight risk-free loans every single day, rolling it over a 10-year horizon. A 10-year treasury yield, on the other hand, reflects also returns from a 10-year term risk-free loan. Here you're committing the principal upfront for 10 years to term. One key difference between these two strategies is this component of terming out your principal and therefore the swap spread basically, to a considerable extent is a reflection of that term funding premium. Swap spreads are also impacted by other factors, liquidity premium, top-term flows, hedging demands from some sector of the market.

My Notes

Here are the key factors that affect swap spreads:

Counterparty Risk, Market Risk, Market Depth, Market Dynamics, Treasury-Specific Factors, Level and Slope of the Yield Curve

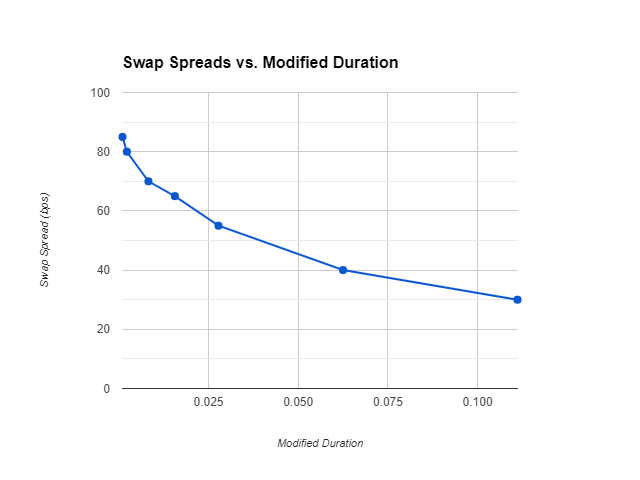

So the question is, how do you extract term funding premium information knowing that these other influences can also exist? And the way we do that is actually we look at the entire term structure. Since term funding premium impacts swap spreads at every maturity, but in a manner that's proportional to its modified duration, you can actually look at the entire term structure and extract this component that is common to all the different maturities. So specifically, imagine taking a snapshot today of swap spreads at every point. You pick every benchmark treasured point. So you pick the twos, threes, fives, sevens, tens, twenties, and thirties, and you plot the maturity match swap spread versus the modified duration of each point.

My Illustration

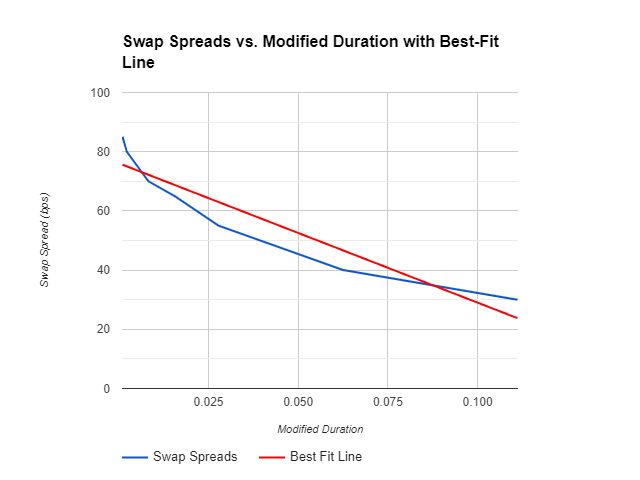

Now imagine drawing the best fit line through this plot. Well, the slope of this line is basically a reflection of term funding premium. The higher the term funding premium, the more steeply inverted the swap spread curve will be.

My Illustration

So that long end spreads will become much more negative relative to front end spreads. So based on that observation, we actually use this link to define term funding premium. Specifically, we define it as basically the negative of the slope of that fitted line. It is our measure of term funding premium, we extract that from not any given swap spread, but from the collection of swap spreads across different maturities. So conversely, you could also say that if we think term funding premium is going higher or lower, that will have an impact on swap spreads at every maturity.

Links term funding premium to supply and demand factors

The supply side, it's relatively easy. It turns out that the best quantification of US Treasury supply for this purpose is to measure Treasury issues in duration weighted units. For example, how many billions of 10 year note equivalents are issued in any given month. So this is the important supply side factor in our model.

We have two demand side factors. The first one is the size of the Fed's balance sheet. So as we know, when the Fed conducts quantitative easing, it does so by purchasing US treasuries. So the balance sheet growth should pressure term funding premium lower and vice versa. We also use aggregate AUM at major bond funds as a second demand side factor.

So using these models, we can also refine our swap spread forecast a little further. And when we put it all together, what we see is that we think swap spreads will likely be biased somewhat wider across much of the curve in the coming months.

Engin YILMAZ (

)

Sources