Maiden Lane I: A Case Study in Financial Crisis Management

Maiden Lane I: A Case Study in Financial Crisis Management

During the catastrophic days of the 2008 financial crisis, The Federal Reserve intervened to prevent the collapse of Bear Stearns by utilizing an economic tool known as Special Purpose Vehicles (SPVs). While SPVs are typically used by private companies for liquidity and other purposes, the Fed's innovative application played a crucial role in stabilizing the financial system.

If you don’t know how Bear Stearns collapsed, you can read from the following link.

March 14, 2008 (Black Friday)

The Board of Governors of the Federal Reserve System authorized the FRBNY to extend credit to Bear Stearns through JPMC. The loan from the FRBNY was for $12.9 billion and was secured by assets valued at $13.8 billion.1 The rate of interest on this loan was the rate for primary credit extended by the Reserve Banks, or 2.25 percent.2 Despite the receipt by Bear Stearns of Federal Reserve funding through the JPMC bridge loan on Friday, March 14, 2008, market pressures on Bear Stearns worsened that day and during the weekend.

March 16, 2008

Bear Stearns accepted an offer to merge with JPMC in a transaction facilitated by the FRBNY. The Federal Reserve created an SPV, which is called Maiden Lane, LLC, (later known as “Maiden Lane I”) to which it lent approximately $29 billion and JPMC lent $1 billion.

If you don’t know how SPV is created and SPV is used, you can read from the following link.

Understanding SPVs: A Beginner's Guide to This Essential Financial Tool (Anatomy of Securitization)

Maiden Lane I: Section13(3)/SPV marriage

A comprehensive look at the Fed’s history with SPVs reveals the oft-postulated story of legal evasion does not hold up.3 The Fed does not have the authority to buy assets other than Treasury securities and a few other types of assets used in open-market operations. If the Fed had simply purchased MBSs and the other toxic assets for $30 billion, it would have violated the law. The transaction was structured to avoid this type of blatant illegality.4 Most special purpose vehicles are structured as limited liability companies, which trace their origin in the United States to the late 1970’s. The Congress that enacted Section 13(3) in the 1930’s envisioned the Federal Reserve lending to companies, but it surely did not envision the Fed lending to an LLC, because that legal form of organization would not be invented for another 40 years.5

“It's easy to think of the SPV as the recipient of the loan and that the Fed is using 13(3) to lend to the SPV. But if you follow that logic, you get to two bad places. One is the Fed lending to the Fed, which is a bad place to be. And the second is then the SPV can hold anything, including real estate, including equity securities...”6

I think where there's no taxpayer money—don't get me wrong: all Fed money.7

Maiden Lane I -The Accounting

1- Bear Stearns accepted an offer to merge with JPMC. This is JPMC’s balance sheet.

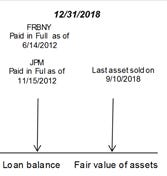

2- The Federal Reserve created an SPV, which is called Maiden Lane, lent it approximately $29 billion (approximately $28.82 billion)

3- The SPV bought the Bear’s mortgages.

4- The last asset sold on 9/10/2018.

Engin YILMAZ (

)References

On Monday morning, March 17, the $12.9 billion back-to-back loan through JPMC Bank to Bear Stearns was repaid in full to the FRBNY with interest of nearly $4 million.

The Legal Position of the Central Bank: The Case of the Federal Reserve Bank of New York Thomas C. Baxter, Jr. Jr., Link

https://crsreports.congress.gov/product/pdf/R/R44185

https://www.imf.org/external/pubs/ft/wp/2009/wp09120.pdf