The Mysterious Fall of SVB: What Really Happened?

The Mysterious Fall of SVB: What Really Happened? The Fall of Silicon Valley's Golden Boys: Behind the Scenes of the SVB Scandal

Key Takeaways:

SVB was the 16th largest bank in the US financial system.

SVB has been ranked among the top 100 in Forbes magazine's 'Best American Banks' list for the past five years.

While 89% of Silicon Valley Bank's customers lacked deposit insurance, only about 42% of total deposits in the United States are uninsured. The total losses by uninsured depositors in the last 30 years has been less than $300 million.

The problem arises from the large amount flow of deposits from SVB's liabilities to the liabilities of another bank. SVB did not have appropriate collateral and operational arrangements in place to obtain liquidity.

The customer base was heavily concentrated in VC-backed technology and life sciences companies.

SVB invested in long-dated, government- or agency-issued mortgage-backed securities..

When the price of long-term bonds started to fall after the Fed raised interest rates, SVB changed their accounting method from AFS to HTM. HTM is a smooth rediscount. Interest is recognized as daily income and does not affect the equity account in any way. Losses and profits are seen as unrealized.

As of December 31, 2022, SVBFG’s total HTM securities portfolio had a weighted-average duration of 6.2 years, and the majority of SVBFG’s HTM portfolio consisted of agency MBS with a maturity of 10 years or more.

The U.S. Treasury’s two-year bonds was close at 4.60 percent, bank depositors meanwhile were still being paid only 0.2 percent on their deposits and this has led to a steady withdrawal of funds from banks – and a corresponding decline in commercial bank balances with the Federal Reserve.

SVBFG benefited from the record-high deposit inflows during rapid VC and tech sector growth, supported in part by a period of exceptionally low interest rates. SVBFG invested those deposits in longer-term securities and did not effectively manage the interest-rate risk, including actively removing hedges as rates were rising.

You can download or read this article as pdf

INTRODUCTION

Silicon Valley Bank Financial Group (SVBFG) was founded in 1983 and was headquartered in Santa Clara, California. SVBFG’s principal subsidiary was Silicon Valley Bank (SVB), a California state-chartered bank.

WHAT HAPPENED ?

Silicon Valley Bank announced1 a plan on March 8, 2023, to restructure its balance sheet. SVB had sold $21 billion in available-for-sale (AFS) securities, was booking a $1.8 billion after-tax loss, was planning to increase term borrowings by $15 billion to $30 billion, and was seeking to raise $2.25 billion in capital.

On March 9, SVB lost over $40 billion in deposits, and SVB management expected to lose over $100 billion more on March 10. This deposit outflow was remarkable in terms of scale and scope and represented roughly 85 percent of the bank’s deposit base2.

Silicon Valley Bank was officially closed by California Department of Financial Protection and Innovation on March 10, 2023, with the following FDIC3 announcement.

SVB Position

SVB was the 16th largest bank in the US financial system. This bank has been ranked among the top 100 in Forbes magazine's 'Best American Banks4' list for the past five years. According to the WSJ5, the three collapsed banks (SVB, Signature and First Republic) held more assets than all 25 banks that failed in 2008 during the global financial crisis.

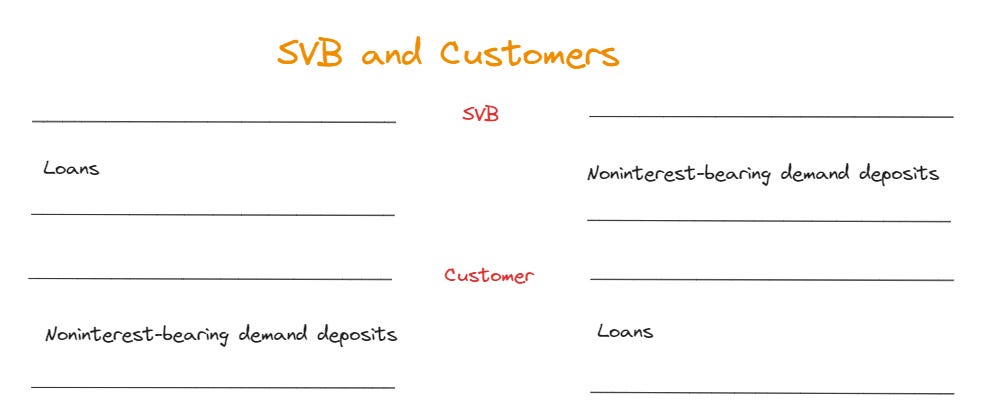

This bank had good relationships with venture capital and startups6 in the US financial system and it mostly granted credits to them instead of collecting deposits. It can see from the SVB’s financial statement in 20237.

Average noninterest-bearing demand deposits: 109,748 in millions $

Average interest-bearing deposits: 76,013 in millions $

We know for certain that 109,748 millions $ in deposits was created by granting credits to these companies.

There are several possibilities regarding the source of these average interest-bearing deposits: one option is that a portion of this amount was converted from non-interest-bearing deposits, and another is that some funds were transferred from other banks with reserves.

Option I: Old noninterest-bearing demand deposits turned to interest-bearing demand deposits

Adam Tooze8 stated that this option is compulsory for some startups with working SVB.

Option II: Some funds were transferred from other banks with reserves.

What is the problem?

The FDIC provides a deposit guarantee of up to $250,000 for customers. You are covered under this guarantee up to that amount.

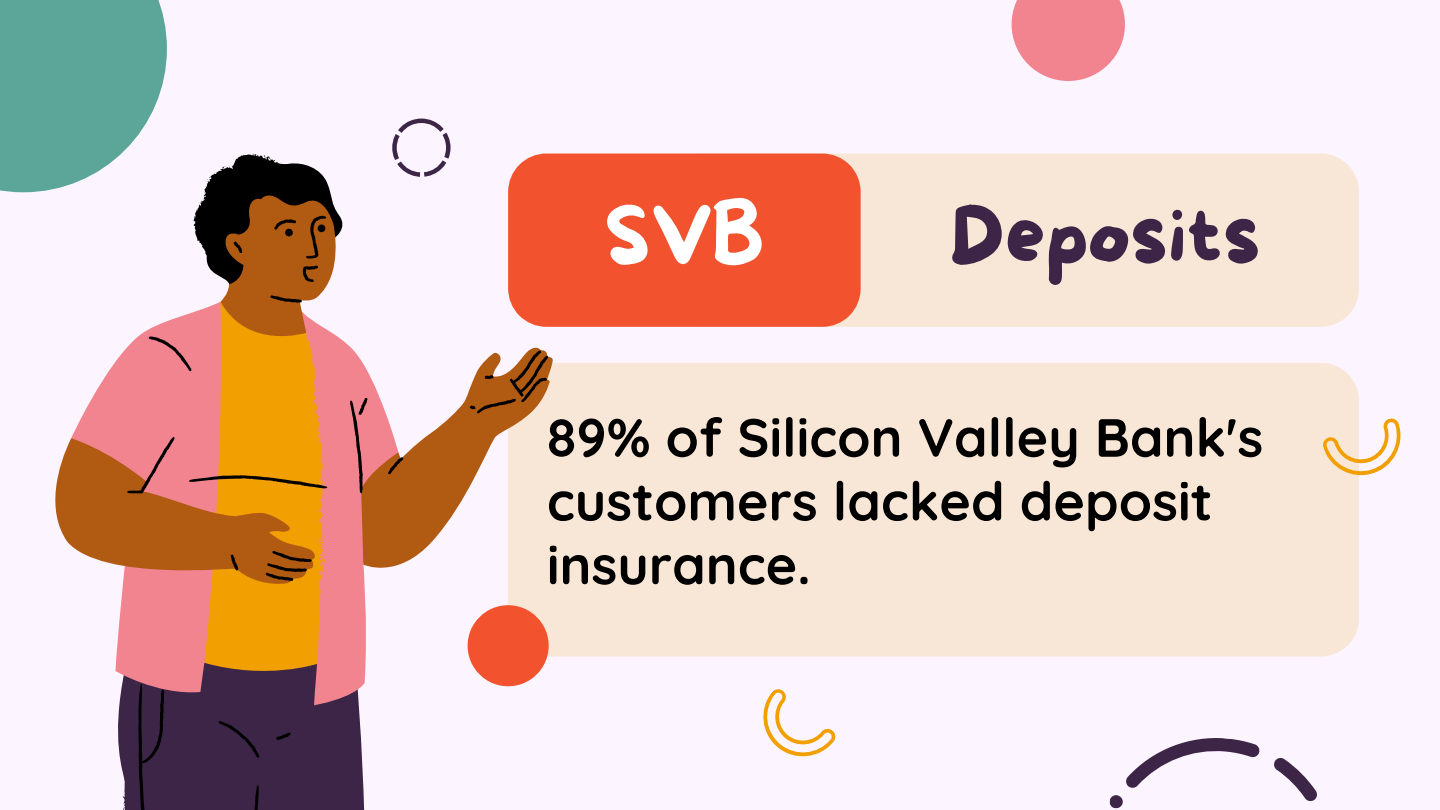

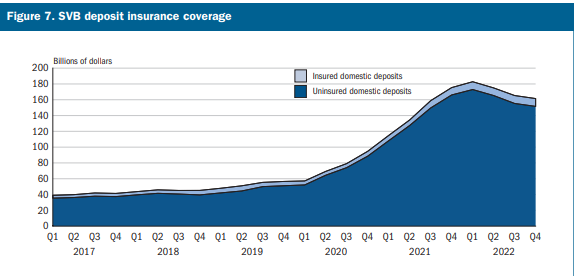

The problem was that 89%9 of SVB’s customers were not covered by this guarantee.

We can conclude that the guarantee is important factor in the banking system. This limit is high enough that the vast majority of all accounts are fully insured, but on a dollar basis, about 42 percent of the total deposits in the United States were above this limit, and thus uninsured (FDIC 2023c, p. 10)10. The total losses by uninsured depositors in the last 30 years has been less than $300 million (FDIC 2023c, p. 22)11.

It is understood there is no problem for uninsured deposits in the US financial system.

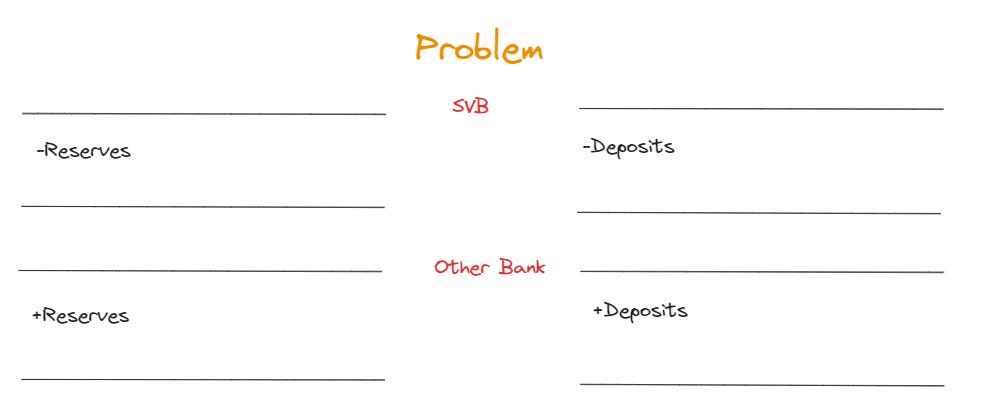

The problem arises from the large amount flow of deposits from SVB's liabilities to the liabilities of another bank.

In its 2023 financial statement (p. 122), SVB reported total cash and cash equivalents amounting to $13.803 billion. This reserve amount is insufficient to cover a large outflow of deposits from the bank.

SVB did not have appropriate collateral and operational arrangements in place to obtain liquidity12.

The customer base was heavily concentrated in VC-backed technology and life sciences companies. VC-backed companies accounted for more than half of SVBFG deposits at year-end 2022, and client funds that SVBFG placed off-balance-sheet were even more concentrated in the same client group This concentration linked SVBFG’s funding growth directly to VC deal activity.

As VC deal activity boomed in 2021 and early 2022, SVBFG’s clients received investment proceeds, which were then deposited at SVB, increasing SVBFG’s deposit levels13.

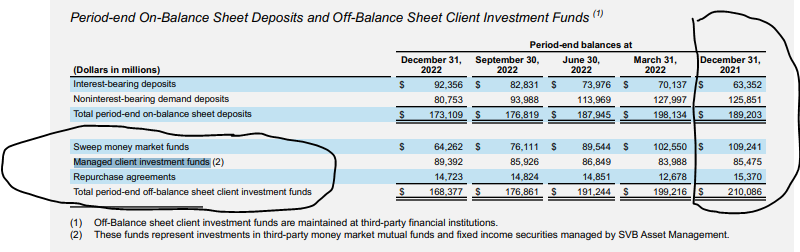

It is simple. SVBFG managed its client investment funds and time, some of these funds were transferred onto the balance sheet. Off-Balance sheet client investment funds are the sweep money market accounts, third-party funds managed by SVB, and repo investments, are “maintained at third-party financial institutions14.”

What is the real problem?

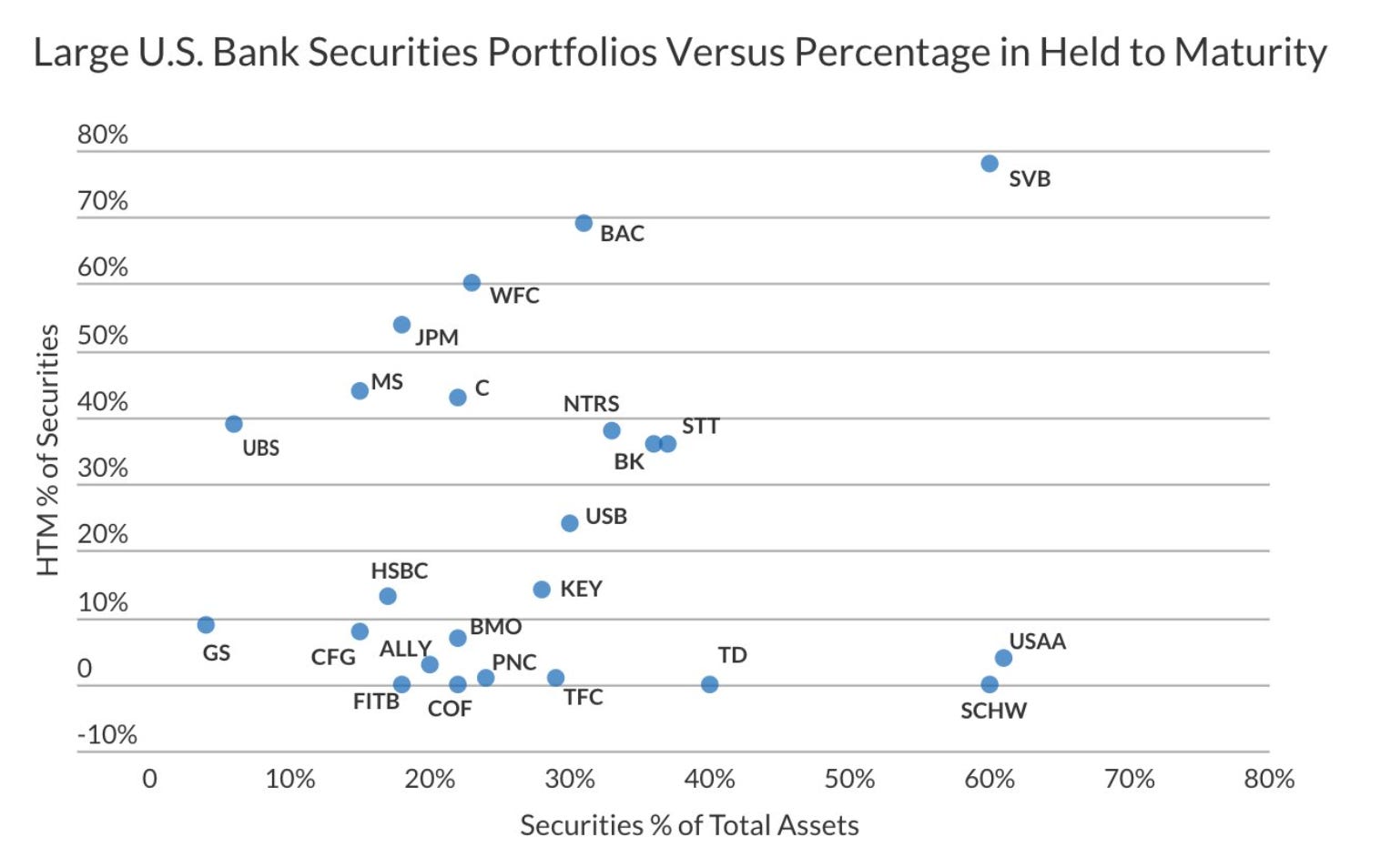

SVBFG chose to invest the long-dated, held-to-maturity (HTM), government or agency-issued mortgage-backed securities (agency MBS).

Allianz Research15 illustrated the SVB balance sheet , which shows how the asset side of SVB is covered by HTM (Held-To-Maturity) type securities. The following graph also shows how SVB's position is heavily concentrated in HTM (Held-To-Maturity) type securities.

As of December 31, 2022, SVBFG’s total HTM securities portfolio had a weighted-average duration of 6.2 years, and the majority of SVBFG’s HTM portfolio consisted of agency MBS with a maturity of 10 years or more.

Classification as HTM enables the securities booked in this fashion to be carried at amortized historical cost rather than at their fluctuating mark-to-market value. Generally, if a bank sells a portion of its HTM portfolio, the entire portfolio would be required to be reclassified as AFS and marked to market.

When the price of long-term bonds started to fall after the Fed raised interest rates, banks changed their accounting method from AFS to HTM. HTM is a smooth rediscount. Interest is recognized as daily income and does not affect the equity account in any way. Losses and profits are seen as unrealized.

SVB continued to play this game for some time by showing the bonds on its balance sheet in the HTM and not reducing its equity. The false spring started to end as the value of the bonds in the bank's asset side started to decline. When the value of these bonds started to decline and the interest to be paid for new time deposits started to increase, a solvency situation began to emerge for the bank.

The U.S. Treasury’s two-year bonds was close at 4.60 percent, bank depositors meanwhile were still being paid only 0.2 percent on their deposits and this has led to a steady withdrawal of funds from banks – and a corresponding decline in commercial bank balances with the Federal Reserve16 . SVB started selling their securities from the balance sheet, but this turned into a fire sale. On Friday(March 10), SVB shares plunged 60 percent after the bank announced a day earlier that it had sold $21 billion in assets and planned to sell some of its shares to raise money.

SVBFG benefited from the record-high deposit inflows during rapid VC and tech sector growth, supported in part by a period of exceptionally low interest rates. SVBFG invested those deposits in longer-term securities and did not effectively manage the interest-rate risk, including actively removing hedges as rates were rising. At the same time, SVBFG failed to manage the risks of its liabilities, which proved much more unstable than anticipated.

A very high percentage of uninsured deposits and significant “unrealized” losses on assets. That combination is a dangerous mix, and variations on it lie at the core of most financial panics17.

Steven Kelly18 stated that “But there were a few dozen banks that were similarly situated that did not fail and did not experience runs. Part of the story is the interest rate sensitivity of SVB’s liabilities. When they came out in March [2023] and said our clients are running down cash balances much faster than we expected, that turned those unrealised losses in the long-term assets into realised losses, because the assets needed to be liquefied. That’s why you can have a Bank of America with $100bn of unrealised losses and nobody is worried, because the business model of Bank of America is strong. If BofA needs capital, they can get it in two seconds, and there is no interest rate sensitivity in their deposits. SVB was dependent on equity flows from venture capital into technology for their deposits. Its funding was macroeconomically sensitive in a way that its supervisors did not recognise. SVB thought they had the most loyal depositors in the world. So when money stopped flowing into tech, which is an interest rate sensitive sector, the liability story for SVB just exploded.”

Kelly 202519

Who caused the collapse of the SVB?

Silicon Valley Bank’s board of directors and management failed to manage their risks.

Supervisors did not fully appreciate the extent of the vulnerabilities as Silicon Valley Bank grew in size and complexity.

When supervisors did identify vulnerabilities, they did not take sufficient steps to ensure that Silicon Valley Bank fixed those problems quickly enough.

Conclusion

The collapse of Silicon Valley Bank (SVB) was largely due to its significant exposure to high-risk, long-term investments and a customer base concentrated in the volatile tech sector. These vulnerabilities were compounded by rapid interest rate increases, which devalued SVB's investments and triggered a massive withdrawal of deposits. The bank's management and regulatory bodies failed to adequately address these risks, leading to a liquidity crisis and ultimately, the bank's abrupt closure. This situation underscores the critical importance of diversified investments, effective risk management, and vigilant oversight in the banking industry.

Engin YILMAZ (

)Sources

FDIC Creates a Deposit Insurance National Bank of Santa Clara to Protect Insured Depositors of Silicon Valley Bank, Santa Clara, California, Link

The Silicon Valley Bank Failure - How tech hubris and low interest rates combined to produce a big mess, Link

FDIC. 2023c. FDIC’s Supervision of Signature Bank. Washington, DC: FDIC.

FDIC. 2023c. FDIC’s Supervision of Signature Bank. Washington, DC: FDIC.

The Failure of Silicon Valley Bank and the Panic of 2023, Andrew Metrick

Steven Kelly, SVB, 2025 https://www.chicagofed.org/publications/working-papers/2025/2025-04

The blog post is all killer, no filler. Keep up the great work.