Do Shadow Banks Create Money ?

Understanding Shadow Banking Through the Monetary Circuit Theory

The liabilities of shadow banks are not money.

The liabilities of shadow banks are not money.

The liabilities of shadow banks are not money.

Here's a very short summary of Jo Michell’s Do shadow banks create money? :

#EconTwitter #MonetaryCircuit #ShadowBanking

Two Views on Shadow Banking

Market View : The market view of shadow banking sees the phenomenon as the rise to dominance of disaggregated market-mediated -financial transactions, and emphasises such activities as dealing in securitised debt. In this view, money and banking are demoted in signi cance relative to arms-length market-mediated financial transactions.

Money View : Argues that shadow banking performs bank-like functions such as maturity and credit transformation.Holders of this view argue that, rather than market intermediation, shadow banking is an extension of banking because shadow banks issue money.

Circuit View

In this paper it is argued that the statement that shadow liabilities are money is not immediately valid from a circuitist perspective because these financial claims cannot be used either as a means of payment for goods and services or as a means of settlement for financial contracts. Rather than money|in the sense of means of payment|the liabilities issued by the shadow banking system are near-monies: liquid short-term stores of wealth. Shadow banks are reliant on traditional banks for the endogenous expansion of credit, while traditional banks rely on the shadow banks as a storage facility for credit claims which exceed the capacity of traditional bank balance sheets.

Key Insights

🤼 It is argued that the statement that shadow liabilities are money is not immediately valid from a circuitist perspective because these financial claims cannot be used either as a means of payment for goods and services or as a means of settlement for financial contracts.

🤼Nonetheless, rather than money “in the sense of means of payment” the liabilities issued by the shadow banking system are near-monies: liquid short-term stores of wealth.

🤼Much of the growing mass of intermediation between ultimate lenders and borrowers, while appearing as arms-length nancial relationships mediated through the shadow banking system, is reliant on the power of commercial banks to endogenously create loans and deposits.

🤼Liquid balances held in the form of the liabilities issued by shadow banks may not be immediately used as means of payment but since they provide a nightly option to convert at par into money proper, they are a close substitute.

🤼Since shadow bank liabilities must be converted into payment systems money before they can be deployed as purchasing power, these liabilities substitute the immediate means of payment function for means of payment one step removed, while retaining the function of liquid store of value. In this respect, shadow bank liabilities have much in common with traditional savings deposits.

Shadow Banking System

The ultimate creditors of the system hold claims on money market mutual funds (MMFs) and large institutional securities lenders such as pension funds. These institutions lend to dealer-brokers and conduits using tri-party repo and asset-backed commercial paper (ABCP). Tri-party repo lending and clearing is done on the balance sheets of the big clearing banks, which also act as custodians for repo collateral. Bilateral repo markets connect dealer-brokers, hedge funds and traditional mortgage lending banks as well as providing a mechanism for inter-bank lending between traditional banks. Dealer-brokers hold the asset-backed paper (ABS) issued by special purpose vehicles (SPFs) which in turn fund securitised mortgages originated by mortgage lending banks.

Shadow banking monetary circuit

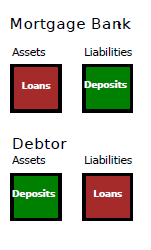

In the first step, the bank lends to a debtor household by issuing a mortgage loan, creating a deposit in the process.

In the second step, the debtor household spends the newly obtained deposit (by purchasing of a house, for example) and the deposit is transferred to the balance sheet of a creditor household.

In the third step, the creditor household doesn't wish to hold a deposit and purchases a share in the MMF. The purchase is made by transferring ownership of the bank deposit from the bank account of creditor household to that of the MMF.

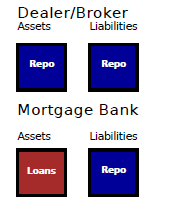

In the fourth step, the MMF has an excess of `cash' and so it uses a repo to lend short-term to a dealer-broker, the MMF exchanges the bank deposit for a repo asset.

In the fifth step, the dealer-broker lends to the mortgage-issuing bank through the bilateral repo market the `interbank' market. This allows the mortgage lending bank to replace the deposit funding of its loanbook with repo funding.

The shadow banking system can be seen as a `loan storage' facility in which money claims are crystallised into less liquid, yet short-term claims which exhibit many features of money, yet are not`money proper'. In the process of transferring credit claims onto the balance sheets of shadow banking institutions, the deposit created when the bank originally made the loan is destroyed, and the monetary circuit closed allowing banks to initiate the circuit once again by creating a new loan and a new deposit, without reducing their (on-balance sheet) liquidity or capital.

In the shadow banking era, the majority of money and credit claims are created when banks lend to households. When this money is spent it ends up either in the hands of wealthy individuals or as corporate profits. Such wealthy individuals or corporations, in turn use the money to buy the liabilities of money market funds or other financial intermediaries. From here, money is passed along the links of the chain until is it used to simultaneously remove a loan from the balance sheet of a bank, and extinguish a deposit. In this way, the monetary circuit has escaped the constraints of real output.